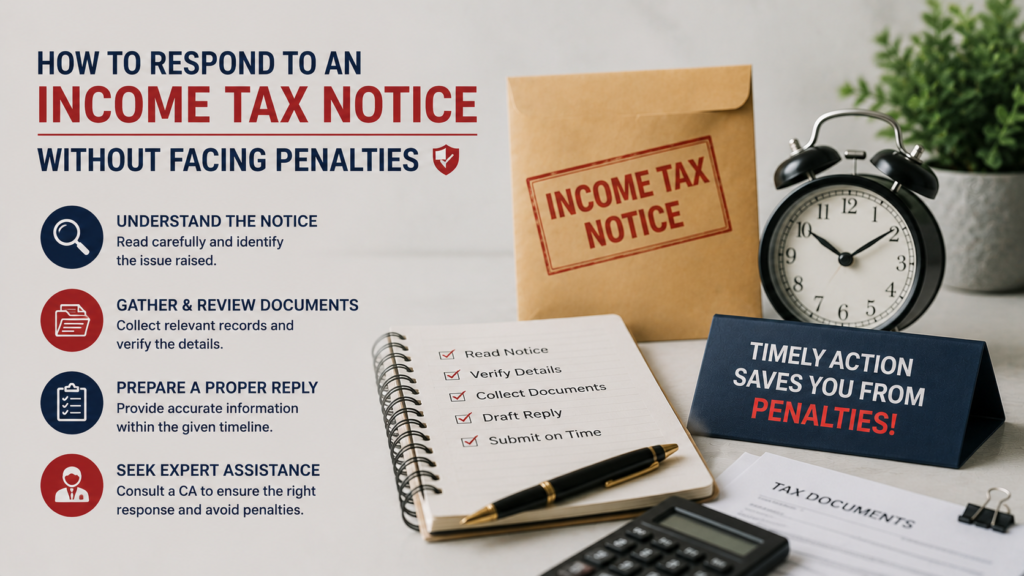

How to Respond to an Income Tax Notice Without Facing Penalties

TL;DR Receiving an Income Tax Notice does not necessarily mean you’ve committed tax fraud. Many notices are issued for routine verification, mismatched information, missing documents, or clarification requests. The key is responding accurately and within the prescribed deadline. Working with an experienced Chartered Accountant can significantly reduce the risk of penalties and ensure smooth compliance. Receiving an Income Tax Notice Isn’t the End—But Ignoring It Can Be Few things create panic for taxpayers like opening an email from the Income Tax Department. Whether you’re a salaried employee, freelancer, startup founder, or business owner, receiving an Income Tax Notice can be stressful. However, it’s important to understand that most notices are not punishments—they’re requests for clarification or verification. The Income Tax Department increasingly relies on technology, AI-based data matching, and analytics to identify discrepancies between your Income Tax Return (ITR), GST filings, TDS records, Annual Information Statement (AIS), and financial transactions. If any mismatch is detected, a notice may be issued. Responding correctly—and on time—is the difference between resolving the issue smoothly and facing unnecessary penalties. Why Does the Income Tax Department Send Notices? Common reasons include: Income mismatch High-value transactions Incorrect deductions claimed Missing income disclosure TDS mismatch AIS mismatch Bank transaction discrepancies Capital gains not reported Late filing Defective ITR Tax audit selection Random scrutiny assessments Receiving a notice doesn’t automatically mean you’ve done something wrong. Common Types of Income Tax Notices Notice Type Purpose Defective Return Errors in ITR filing Scrutiny Notice Detailed examination of return Demand Notice Additional tax payable Reassessment Notice Previously undisclosed income Information Request Clarification regarding transactions Notice for Non-Filing Return not filed despite eligibility Each notice has different timelines and documentation requirements. Step 1: Stay Calm and Read the Notice Carefully Avoid reacting emotionally. Instead: Read every page. Check the section under which the notice is issued. Verify the Assessment Year. Note the response deadline. Understand exactly what information is requested. Many taxpayers respond incorrectly simply because they misunderstand the purpose of the notice. Step 2: Verify the Authenticity Before responding: Log into the Income Tax e-Filing Portal. Check whether the notice appears under your account. Match the Document Identification Number (DIN). Confirm the issuing officer’s details. Never respond to suspicious emails without verification. Step 3: Identify the Reason for the Notice The reason determines your response. Examples include: Income mismatch Perhaps your employer reported different salary figures. TDS mismatch Tax deducted may not reflect correctly. AIS mismatch Banks, mutual funds, brokers, or employers may have reported transactions differently. High-value transactions Examples: Property purchase Luxury vehicle purchase Large cash deposits Foreign travel Credit card spending The department simply seeks clarification. Step 4: Gather Supporting Documents Prepare all relevant records before submitting your response. These may include: PAN Aadhaar Income Tax Returns Form 16 Form 26AS Annual Information Statement (AIS) Bank Statements Investment Proofs Capital Gain Statements GST Returns Purchase Invoices Sale Bills Audit Reports Loan Documents Business Books of Accounts Organized documentation leads to faster resolution. Step 5: Draft a Clear and Accurate Response Your response should: Answer every query. Attach supporting documents. Be factual. Avoid assumptions. Avoid emotional explanations. Reference supporting evidence. A professional, structured reply significantly improves credibility. Step 6: Submit Before the Deadline Late responses often lead to: Penalties Interest Best judgment assessment Additional notices Prosecution in severe cases Always submit well before the due date to avoid technical issues. Step 7: Track the Status After submission: Save the acknowledgement. Monitor the Income Tax Portal. Respond quickly if additional clarification is requested. Tax proceedings may involve multiple rounds of communication. Common Mistakes That Can Lead to Penalties Many penalties arise not because of tax evasion, but because of avoidable errors such as: Ignoring the notice. Missing response deadlines. Uploading incomplete documents. Providing inaccurate information. Contradicting previously filed returns. Failing to reconcile AIS or Form 26AS data. Responding without professional review. A careful, evidence-based reply can prevent unnecessary complications and improve the chances of a quick resolution. Step 8: Seek Professional Assistance When Required While some basic notices can be handled independently, complex notices involving scrutiny, reassessment, high-value transactions, or tax demands require expert guidance. A qualified Chartered Accountant can: Interpret the legal provisions mentioned in the notice. Review your Income Tax Return for inconsistencies. Reconcile data with Form 26AS, AIS, and TIS. Prepare a legally sound response. Represent you before the Income Tax Department when required. Help minimize additional tax liabilities, interest, or penalties. Professional assistance not only saves time but also reduces the risk of making errors that could escalate the matter. Can a Chartered Accountant Respond to an Income Tax Notice on Your Behalf? Yes. A Chartered Accountant can represent taxpayers in many tax-related matters, depending on the nature of the notice and the applicable provisions under the Income-tax Act. A CA can assist with: Drafting detailed responses. Preparing supporting documentation. Reconciling tax records. Filing revised or updated returns, where applicable. Representing the taxpayer during assessments. Communicating with the Income Tax Department. For businesses and professionals with complex financial transactions, having expert representation often leads to a smoother resolution. How to Avoid Penalties After Receiving an Income Tax Notice The best way to avoid penalties is to respond proactively and accurately. Follow these best practices: ✔ Reply Before the Deadline Never wait until the last day. Early responses leave time to address any technical issues or additional requests. ✔ Submit Complete Information Incomplete responses often result in follow-up notices and prolonged assessments. ✔ Match All Financial Records Ensure consistency between: Income Tax Return (ITR) Form 26AS Annual Information Statement (AIS) Taxpayer Information Summary (TIS) GST Returns (if applicable) Bank statements Books of accounts ✔ Keep Supporting Documents Ready Maintain organized records for at least the prescribed retention period to respond quickly if questioned. ✔ Be Honest and Transparent If an error was made, acknowledge it and provide the correct information. Intentional concealment can attract more severe consequences than an honest mistake. ✔ Consult a Chartered Accountant Professional review helps identify risks before submitting your reply and ensures

Why Every Startup Needs a Chartered Accountant Before Raising Funds

TL;DR A great business idea alone is rarely enough to secure funding. Investors expect startups to demonstrate financial discipline, legal compliance, accurate reporting, and realistic growth projections. A Chartered Accountant (CA) plays a crucial role in preparing your startup for fundraising by ensuring your financial records are investor-ready, identifying compliance gaps, assisting with valuation, and supporting due diligence. Engaging a CA before approaching investors can significantly improve your chances of raising capital while avoiding costly mistakes. Why Raising Funds Is More Than Just Pitching an Idea Many founders believe that a compelling pitch deck and an innovative product are enough to attract investors. While these elements are important, experienced investors place equal—if not greater—importance on a startup’s financial health and operational readiness. Whether you’re approaching angel investors, venture capital firms, banks, or government funding programs, you’ll be expected to provide accurate financial information and demonstrate that your business is built on a strong financial foundation. Investors are not simply investing in an idea—they are investing in a business that can manage capital responsibly and deliver sustainable returns. This is where the expertise of a Chartered Accountant becomes invaluable. What Investors Expect Before Funding Before committing capital, investors conduct detailed evaluations to assess both the opportunities and risks associated with your startup. 1. Accurate Financial Statements Investors want confidence that your reported numbers reflect the true financial position of your business. Typically requested documents include: Profit & Loss Statement Balance Sheet Cash Flow Statement Revenue reports Expense analysis Bank reconciliations Financial ratios Poorly maintained accounts immediately raise concerns about governance and operational discipline. 2. Complete Regulatory Compliance Investors carefully examine whether the startup complies with applicable legal and tax requirements. Common areas reviewed include: Income Tax filings GST compliance TDS compliance ROC filings (where applicable) Accounting records Payroll compliance Statutory registrations Even minor compliance lapses can delay or jeopardize funding discussions. 3. Reliable Financial Forecasts Funding decisions are based largely on future growth potential rather than past performance. Investors expect realistic projections covering: Revenue growth Operating expenses Cash burn Customer acquisition costs Gross margins Profitability timelines Capital utilization A Chartered Accountant helps develop forecasts based on realistic assumptions rather than optimistic estimates. 4. Transparent Business Operations Transparency builds investor confidence. Founders should be prepared to explain: Revenue model Cost structure Pricing strategy Outstanding liabilities Existing debt Related-party transactions Capital structure Well-organized documentation reflects professionalism and reduces perceived investment risk. How a Chartered Accountant Helps Before Fundraising A Chartered Accountant contributes far beyond tax filing. They act as a strategic financial advisor throughout the fundraising journey. 1. Preparing Investor-Ready Financial Statements One of the first tasks of a CA is organizing the startup’s financial records into professional, accurate reports. This includes: Cleaning bookkeeping records Reconciling bank accounts Verifying assets and liabilities Preparing audited or reviewed statements (where applicable) Standardizing accounting practices Clear financial statements improve credibility during investor meetings. 2. Ensuring Tax Compliance Tax-related issues are among the most common reasons investors request additional clarification during due diligence. A CA ensures: GST returns are filed correctly Income Tax returns are updated TDS obligations are fulfilled Advance tax liabilities are addressed Tax notices are resolved proactively Strong tax compliance demonstrates financial discipline and minimizes legal risks. 3. Assisting with Startup Valuation Valuation determines how much equity founders may need to dilute in exchange for investment. A Chartered Accountant supports valuation by analyzing: Revenue performance Profitability trends Cash flows Comparable businesses Industry benchmarks Asset values Growth projections Accurate valuation helps founders negotiate confidently and avoid unnecessary dilution. 4. Preparing for Financial Due Diligence Due diligence is a detailed examination of every significant financial and legal aspect of the startup. A CA helps organize: Financial statements Tax filings Shareholding records Compliance certificates Loan agreements Vendor contracts Customer agreements Statutory registers Being due diligence-ready shortens fundraising timelines and builds investor trust. 5. Building Realistic Financial Projections One of the biggest mistakes founders make is presenting unrealistic revenue forecasts. A Chartered Accountant prepares evidence-based projections using: Historical financial data Industry growth trends Market assumptions Cost estimates Pricing models Cash flow planning Break-even analysis Credible financial projections reassure investors that management understands the economics of the business. 6. 10 Ways a Chartered Accountant Increases Your Startup’s Funding Success A Chartered Accountant does much more than prepare tax returns. They become a strategic financial partner who helps startups present a strong investment case. 1. Builds Investor Confidence Investors trust startups with organized financial records, transparent accounting practices, and complete statutory compliance. Professionally maintained books indicate that the founders are capable of managing investment responsibly. 2. Improves Financial Reporting A CA ensures your financial reports are accurate, timely, and aligned with accepted accounting standards. This includes: Profit & Loss Statements Balance Sheets Cash Flow Statements Management reports Monthly financial dashboards Clear reporting makes investor discussions smoother. 3. Reduces Compliance Risks Non-compliance with GST, Income Tax, TDS, or ROC requirements can become major red flags during due diligence. A Chartered Accountant helps eliminate these risks before investors discover them. 4. Assists in Business Valuation Incorrect valuation can either discourage investors or cause founders to dilute excessive equity. A CA helps determine a fair valuation using: Financial performance Comparable companies Future revenue projections Industry benchmarks Growth potential 5. Optimizes Cash Flow Management Investors closely evaluate whether startups can efficiently manage cash. A Chartered Accountant helps: Monitor cash burn Improve working capital Control unnecessary expenses Forecast funding requirements Plan future capital allocation 6. Strengthens Internal Controls Good internal controls reduce financial fraud and operational risks. Examples include: Approval systems Expense policies Vendor verification Financial documentation Audit trails 7. Supports Better Tax Planning Effective tax planning improves profitability and investor returns without violating tax regulations. A CA identifies: Eligible deductions Tax-saving opportunities Incentives available for startups Efficient business structures 8. Prepares a Due Diligence Data Room Professional investors expect a well-organized virtual data room containing all essential documents. A Chartered Accountant helps prepare: Financial statements Tax returns Compliance certificates Shareholding records Contracts Licenses Payroll records 9. Helps Negotiate Investor Discussions Financial negotiations

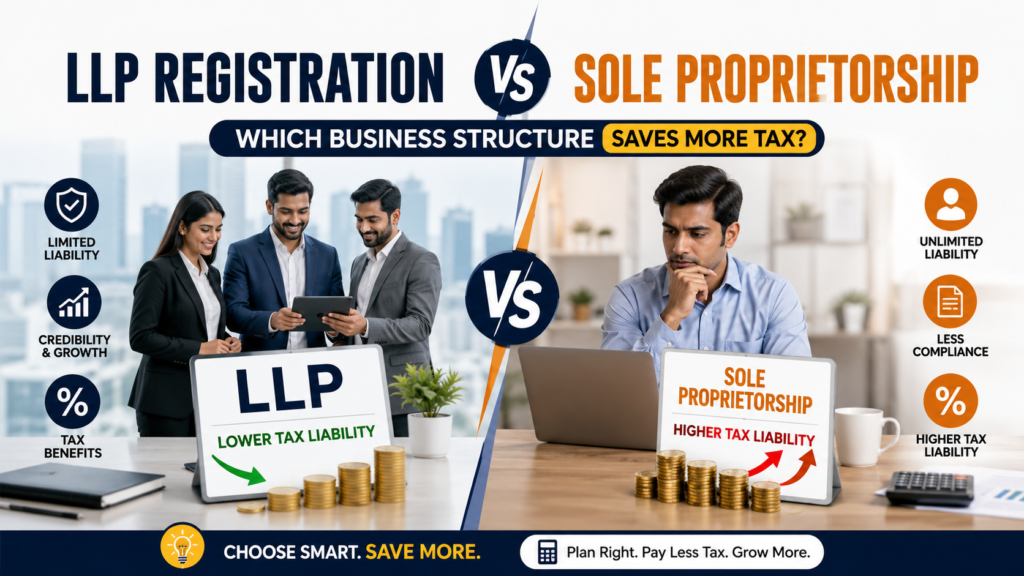

LLP Registration vs Sole Proprietorship: Which Business Structure Saves More Tax?

TL;DR If you’re starting a business in India, choosing between an LLP and a Sole Proprietorship can significantly impact your taxes, legal liability, compliance burden, and future growth. While a Sole Proprietorship offers simplicity and lower compliance, an LLP provides limited liability, greater credibility, and better scalability. The right choice depends on your business goals, expected profits, and expansion plans. Why Choosing the Right Business Structure Matters One of the biggest mistakes new entrepreneurs make is selecting a business structure based solely on registration cost or convenience. However, the legal structure of your business affects nearly every aspect of operations—from taxation and compliance to fundraising and risk management. A business that starts as a small proprietorship may later require conversion into an LLP or company due to growth, increasing compliance requirements, or investor expectations. Making the right decision early can save both money and administrative effort. Before registering your business, evaluate factors such as annual turnover, projected profits, number of owners, funding requirements, liability exposure, and long-term business plans. Understanding Sole Proprietorship A Sole Proprietorship is the simplest and most common business structure in India. It is owned and managed by a single individual, and there is no legal distinction between the owner and the business. Key Features Single owner Easy to start Minimal legal formalities Low compliance burden Complete control over business decisions Advantages Low setup cost Simple tax filing Quick business commencement Full control over profits Minimal regulatory requirements Disadvantages Unlimited personal liability Difficult to raise investment Limited business credibility Business ends with the owner Personal assets remain exposed to business risks Understanding LLP Registration A Limited Liability Partnership (LLP) combines the operational flexibility of a partnership with the legal protection of a corporate entity. Unlike a Sole Proprietorship, an LLP is a separate legal entity, meaning the partners’ personal assets are generally protected from business liabilities. Key Features Separate legal identity Minimum two designated partners Limited liability protection Perpetual succession Recognized under the LLP Act Advantages Better business credibility Easier access to funding Legal protection for partners Structured ownership Suitable for growing businesses Disadvantages Annual compliance requirements Mandatory statutory filings Slightly higher registration costs Requires at least two partners LLP Registration vs Sole Proprietorship: Complete Comparison Feature Sole Proprietorship LLP Legal Status Owner and business are the same Separate legal entity Owners One Minimum two partners Liability Unlimited Limited Registration Relatively simple Mandatory LLP registration Taxation Individual tax slab LLP taxation provisions Compliance Low Moderate Fundraising Difficult Easier Business Continuity Depends on owner Perpetual succession Brand Credibility Moderate High Expansion Limited Excellent Tax Comparison Between LLP and Sole Proprietorship Taxation is one of the most important considerations when choosing a business structure. Sole Proprietorship Business income is treated as the owner’s personal income and taxed according to the applicable individual income tax slab. As profits increase, the effective tax burden may also increase depending on the owner’s total taxable income. Suitable for: Freelancers Small traders Local businesses Consultants with modest profits LLP An LLP is taxed under the Income Tax Act as a separate entity. It offers opportunities for structured financial planning and may be more suitable for businesses with consistent profits, multiple partners, or expansion plans. Suitable for: Professional firms Agencies Manufacturers Service companies Growing startups Compliance Comparison Compliance obligations are another important factor when deciding between an LLP and a Sole Proprietorship. While many entrepreneurs focus on tax savings, ongoing regulatory responsibilities can significantly affect operating costs and administrative workload. Compliance Area Sole Proprietorship LLP Income Tax Return Mandatory Mandatory GST Returns (if applicable) Mandatory Mandatory Annual MCA Filing Not Applicable Mandatory Statutory Records Minimal Mandatory Audit Requirement Based on applicable tax/GST provisions Based on applicable legal provisions Separate PAN Uses proprietor’s PAN Separate PAN for LLP Bank Account In proprietor’s name/business name Separate LLP bank account Sole Proprietorship Compliance Compliance is relatively simple and usually includes: Income Tax Return filing GST return filing (if registered) TDS compliance (if applicable) Maintaining basic books of accounts Renewal of local business registrations, where applicable This makes it suitable for businesses with straightforward operations and limited transactions. LLP Compliance An LLP requires more structured compliance, including: Annual Return filing Statement of Accounts and Solvency Income Tax Return GST compliance (where applicable) TDS compliance Maintenance of statutory books and records Partner-related documentation and resolutions Although compliance costs are higher, they improve transparency, governance, and business credibility. Registration Cost Comparison Registration expenses should not be the only deciding factor. Instead, evaluate the total long-term value offered by each business structure. Expense Sole Proprietorship LLP Registration Cost Lower Moderate Annual Compliance Cost Lower Higher Accounting Cost Lower Moderate Legal Protection Limited High Growth Potential Moderate High Many businesses initially choose a proprietorship because of lower costs but later incur additional expenses when converting to an LLP after business growth. Planning ahead can reduce unnecessary restructuring costs. Which Business Structure Is Best for Different Businesses? Choose a Sole Proprietorship if you are: A freelancer A consultant working independently A small retail shop owner Running a home-based business Testing a new business idea Operating with limited investment Choose an LLP if you are: Starting a business with one or more partners Expecting rapid business growth Providing professional services Planning to apply for larger business loans Looking for better credibility with clients Seeking long-term expansion opportunities When Should You Convert a Sole Proprietorship into an LLP? Many successful businesses begin as proprietorships and later convert into LLPs. Consider conversion when: Business turnover increases significantly You add business partners Personal liability becomes a concern Banks require a more formal business structure Clients prefer working with registered entities You plan to expand into multiple cities You want stronger legal protection for personal assets Early planning with a Chartered Accountant ensures the transition is smooth and compliant. Common Mistakes to Avoid Entrepreneurs often make costly decisions by overlooking the broader implications of business structure selection. Avoid these mistakes: Choosing solely based on registration cost Ignoring future tax implications Underestimating compliance requirements Failing to consider liability protection

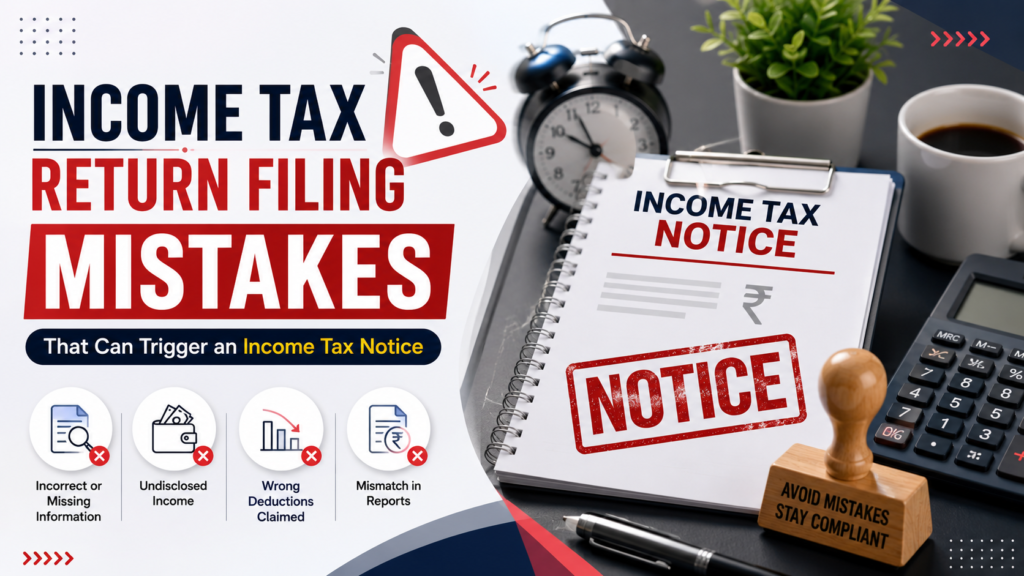

Income Tax Return Filing Mistakes That Can Trigger an Income Tax Notice

TL;DR A single mistake in your Income Tax Return (ITR)—such as underreporting income, claiming incorrect deductions, or mismatching information with AIS or Form 26AS—can result in an Income Tax notice. This guide explains the most common filing errors, how to avoid them, and why working with an experienced Chartered Accountant can help individuals and businesses stay compliant and reduce tax-related risks. Introduction Income Tax Return filing has become significantly more data-driven in recent years. The Income Tax Department now cross-verifies information from multiple sources, including bank transactions, TDS records, Annual Information Statement (AIS), Taxpayer Information Summary (TIS), GST filings, mutual fund transactions, and property registrations. This advanced digital verification system means even small inconsistencies can attract scrutiny. While receiving an Income Tax notice does not automatically imply wrongdoing, responding to notices can be time-consuming, stressful, and expensive if proper documentation is unavailable. Whether you are a salaried employee, freelancer, business owner, contractor, or startup founder, understanding the most common Income Tax Return filing mistakes can help you avoid unnecessary notices and maintain complete tax compliance. Why Income Tax Notices Are Increasing The Income Tax Department now relies heavily on technology and data analytics rather than random assessments. Modern systems compare information from various financial databases to identify discrepancies. Some commonly matched data sources include: Annual Information Statement (AIS) Form 26AS Taxpayer Information Summary (TIS) GST returns PAN-linked banking transactions Property purchase and sale records Securities transactions Mutual fund investments Foreign remittances Credit card spending Because of this integrated approach, omissions that may have gone unnoticed in the past are now detected much more efficiently. How the Income Tax Department Detects Errors The Department compares information reported by taxpayers with data received from banks, employers, financial institutions, registrars, and other reporting entities. Important verification tools include: Annual Information Statement (AIS) Contains details of: Salary Interest income Dividend income Mutual fund investments Share transactions Property transactions Foreign remittances Form 26AS Shows: TDS deducted Advance tax Self-assessment tax Tax collected at source (TCS) GST Records Business turnover declared under GST is often compared with turnover declared in Income Tax Returns. PAN-Based Reporting Every significant financial transaction linked to PAN becomes part of the taxpayer’s financial profile. 15 Income Tax Return Filing Mistakes That Can Trigger an Income Tax Notice 1. Not Reporting All Sources of Income Many taxpayers report only salary income while forgetting: Savings account interest Fixed deposit interest Rental income Dividend income Freelancing income Commission Side business income Even small amounts reflected in AIS should be disclosed appropriately. 2. Mismatch Between AIS and ITR One of the most common reasons for notices is inconsistency between: AIS Form 26AS Filed ITR Before filing, carefully verify every reported transaction. 3. Selecting the Wrong ITR Form Using an incorrect ITR form may result in: Defective return notices Delayed processing Requirement to file again Always choose the return form applicable to your income category. 4. Incorrect Bank Account Details Incorrect account information may delay: Refund processing Verification Communication from the department Ensure all active bank accounts are correctly reported. 5. Claiming Deductions Without Supporting Documents Improper claims under sections such as: 80C 80D Home loan deductions Donations without valid documentation can trigger verification. Maintain: Premium receipts Investment proofs Donation certificates Loan statements 6. Ignoring Capital Gains Many taxpayers mistakenly assume that if no money is withdrawn, taxes do not apply. Capital gains may arise from: Shares Mutual funds Property sales Gold Digital assets These transactions should be reported accurately, even if tax liability is minimal. 7. Incorrect HRA Claims Claiming House Rent Allowance without: Paying rent Rent receipts PAN of landlord (where applicable) can lead to scrutiny. 8. Not Reporting Foreign Assets or Overseas Income Residents holding: Foreign bank accounts Overseas investments Foreign shares Foreign property must disclose these appropriately under applicable schedules. Failure to report can attract significant penalties. 9. Cash Deposit Mismatch Large cash deposits that do not align with declared income often invite queries. Maintain documentation explaining: Business receipts Sale proceeds Agricultural income Gifts (where applicable) 10. Claiming Excessive Business Expenses Businesses sometimes classify personal expenses as business expenses. Common examples include: Personal travel Family expenses Personal vehicle costs Non-business purchases Keep proper invoices and maintain separate personal and business accounts. 11. GST Turnover Does Not Match Income Tax Return Businesses registered under GST should ensure consistency between: GST returns Books of accounts Profit & Loss statement Income Tax Return Large variations frequently trigger scrutiny. 12. Claiming Wrong TDS Credit Never claim TDS that does not appear in: Form 26AS AIS Incorrect TDS claims often delay refunds and may result in notices. 13. Filing Return After Due Date Late filing may result in: Interest Late fees Loss of certain benefits Higher scrutiny in some cases Timely filing demonstrates better compliance. 14. Submitting Fake Investment Proofs Submitting fabricated deductions or manipulated documents is a serious compliance violation and may attract penalties and prosecution under applicable tax laws. Always maintain genuine documentation. 15. Ignoring Mistakes Instead of Filing a Revised Return If you discover an error after filing: Do not wait for a notice. File a revised return within the permitted timeline. Voluntary correction is generally preferable to departmental detection. Quick Checklist Before Filing Your ITR ✔ Verify AIS thoroughly ✔ Match Form 26AS ✔ Reconcile TDS ✔ Report every source of income ✔ Verify bank details ✔ Review capital gains ✔ Check GST turnover (for businesses) ✔ Maintain deduction proofs ✔ Use the correct ITR form ✔ Get professional review before submission Why Businesses Should Hire a Chartered Accountant Income tax laws continue to evolve, making professional guidance increasingly valuable. An experienced Chartered Accountant can help you: Select the correct ITR form Reconcile AIS and Form 26AS Identify eligible deductions Minimize tax liability legally Ensure GST and Income Tax consistency Handle notices and scrutiny professionally Maintain proper financial records Plan taxes proactively instead of reactively Professional tax advice reduces compliance risks while saving valuable time. How Junaid Khan & Co. Helps At Junaid Khan & Co., Chartered Accountants in Bhopal, we assist

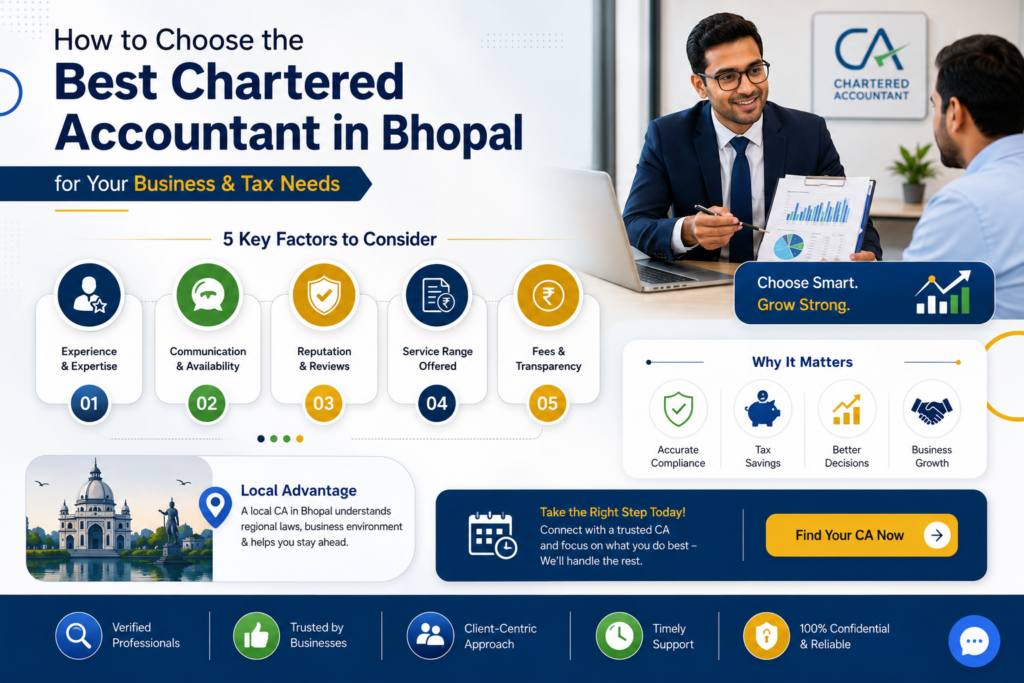

How to Choose the Best Chartered Accountant in Bhopal for Your Business and Tax Needs

TL;DR Choosing the best Chartered Accountant in Bhopal is one of the most important decisions for your business or personal finances. A qualified CA can help you save taxes legally, ensure timely compliance, avoid penalties, improve profitability, and guide your business through every stage of growth. This guide explains exactly what to look for before hiring a Chartered Accountant and how to make the right choice. Why Choosing the Right Chartered Accountant Matters Many business owners think a Chartered Accountant’s role is limited to filing income tax returns. In reality, a professional CA acts as your financial advisor, compliance expert, and strategic business partner. Whether you run a startup, retail shop, manufacturing unit, consultancy, or service business, financial decisions directly impact profitability and long-term growth. The right CA helps you: Reduce tax liability legally Maintain accurate books of accounts Ensure GST compliance Avoid penalties Prepare for audits Improve cash flow Assist with funding and loans Support business expansion Hiring an experienced Chartered Accountant early can save your business significant time, money, and compliance risks. What Does a Chartered Accountant Actually Do? A modern Chartered Accountant provides much more than tax filing. Tax Planning Tax planning is about minimizing your tax burden while remaining fully compliant with Indian tax laws. Professional tax planning includes: Income tax planning Advance tax calculation Capital gains planning Tax-saving investment guidance Business expense optimization Tax notice assistance GST Compliance GST regulations continue to evolve, making professional guidance essential. A CA assists with: GST registration GST return filing Input Tax Credit reconciliation GST audits GST notices GST advisory Accounting Services Proper accounting helps businesses make informed financial decisions. Services include: Bookkeeping Bank reconciliation Financial statements MIS reporting Cash flow analysis Payroll accounting Audit Services Businesses often require professional audit support for statutory and regulatory compliance. Common audit services include: Statutory Audit Tax Audit Internal Audit Stock Audit Due Diligence Compliance Audit Business Registration Launching a business involves multiple legal formalities. A Chartered Accountant can assist with: Private Limited Company Registration LLP Registration Partnership Firm Registration MSME Registration Startup India Registration PAN & TAN GST Registration Financial Advisory Beyond compliance, experienced CAs provide strategic financial guidance. Examples include: Business restructuring Profitability analysis Budget planning Financial forecasting Investment planning Loan documentation Working capital management 10 Factors to Consider Before Hiring a Chartered Accountant 1. Industry Experience Every industry has unique financial and tax requirements. For example: Manufacturing businesses face inventory valuation challenges. Healthcare professionals require specialized tax planning. E-commerce companies manage multi-state GST compliance. Startups need funding support and investor-ready financial statements. Choose a CA who understands your industry rather than one offering only generic accounting services. 2. Complete Range of Services Hiring separate professionals for accounting, GST, taxation, audits, and registrations often increases costs and creates coordination issues. Instead, look for a CA firm offering comprehensive services such as: Accounting Income Tax GST Audit Company Registration ROC Compliance Payroll Financial Advisory Business Consulting A single point of contact simplifies financial management and ensures consistent compliance. 3. Strong Knowledge of Changing Tax Laws Indian tax regulations are updated frequently. A reliable Chartered Accountant should stay current with: Income Tax amendments GST notifications MCA compliance ROC regulations TDS provisions Startup incentives MSME benefits Proactive advice helps businesses adapt quickly and avoid costly mistakes. 4. Technology and Automation Modern accounting is increasingly digital. A capable CA should leverage cloud-based accounting software, secure document sharing, automated compliance reminders, and real-time financial reporting to improve efficiency and accuracy. Businesses benefit from faster reporting, better collaboration, and reduced paperwork when their CA embraces technology rather than relying solely on manual processes. 5. Communication and Responsiveness Financial matters often require timely decisions. Your Chartered Accountant should respond promptly to queries, explain complex concepts in simple language, and keep you informed about important deadlines and regulatory changes. Poor communication can lead to missed compliance dates and unnecessary penalties. 6. Reputation and Client Reviews Before finalizing a Chartered Accountant, research their reputation thoroughly. Consider: Google reviews and ratings Client testimonials Years of experience Industry recognition Case studies Referral recommendations Consistent positive feedback often reflects professionalism, reliability, and long-term client satisfaction. 7. Transparent Pricing The cheapest CA is not always the best choice. Instead, look for: Clearly defined service packages Transparent fee structure No hidden charges Defined scope of work Annual compliance plans Ongoing advisory support Choosing based on overall value rather than price alone usually delivers better long-term results. 8. Personalized Business Advice Every business has unique financial goals and compliance requirements. A good Chartered Accountant should: Understand your business model Identify potential risks Recommend tax-saving opportunities Improve financial processes Support business expansion Offer proactive advice throughout the year Avoid professionals who only become available during tax season. 9. Scalability of Services As your business grows, your compliance and financial needs become more complex. Choose a CA firm that can support: Company incorporation Multi-state GST Payroll management Internal audits Investor reporting Funding assistance Business valuation Expansion planning Working with a scalable firm eliminates the need to switch advisors as your business evolves. 10. Long-Term Partnership Approach The best Chartered Accountant is more than a compliance expert—they become a strategic business advisor. A long-term relationship enables your CA to: Understand your financial history Anticipate future challenges Recommend growth strategies Improve profitability Ensure ongoing compliance Provide timely financial insights This continuity leads to better financial planning and stronger business outcomes. Questions You Must Ask Before Hiring a Chartered Accountant Before making your decision, ask: How many years of experience do you have? Do you work with businesses in my industry? Which accounting software do you use? What services are included in your engagement? How frequently will we communicate? Who will be my primary point of contact? How do you handle tax notices or assessments? What is your typical turnaround time? How are your fees structured? Can you support future business expansion? These questions help you assess expertise, communication style, and long-term compatibility. Red Flags to Avoid Be cautious if a CA: Promises unrealistic tax savings Lacks transparency in

GST Registration vs Composition Scheme: Which Is Better for Small Businesses in Bhopal?

TL;DR If your business has growth ambitions, works with corporate clients, wants Input Tax Credit benefits, or operates across multiple states, Regular GST Registration is usually the better option. If your business is small, locally focused, has limited compliance capacity, and wants simplified taxation, the Composition Scheme may be suitable. The right choice depends on: ✔ Annual turnover ✔ Customer type ✔ Profit margins ✔ Growth plans ✔ Compliance capability ✔ GST Input Tax Credit requirements This guide explains both options in detail to help Bhopal business owners make an informed decision. Why This Decision Matters More Than Ever For many small businesses in Bhopal, GST compliance is no longer just a legal requirement—it directly affects profitability, cash flow, pricing strategy, and business growth. One of the most common questions business owners ask is: “Should I register under the normal GST scheme or opt for the Composition Scheme?” Choosing the wrong option can lead to: Higher tax costs Reduced competitiveness Limited growth opportunities Compliance challenges Cash flow issues On the other hand, selecting the right scheme can simplify operations and improve profitability. Let’s break down both options. Understanding Regular GST Registration Regular GST Registration is the standard GST framework under which businesses collect GST from customers and remit it to the government. Businesses registered under the regular scheme can: Charge GST on invoices Claim Input Tax Credit (ITC) Conduct interstate business Sell through e-commerce platforms Supply goods and services to corporate clients Participate in government tenders This scheme is generally designed for businesses that expect growth and need operational flexibility. Key Features of Regular GST Registration Input Tax Credit Available One of the biggest advantages is the ability to claim GST paid on purchases. For example: If a trader purchases inventory worth ₹10 lakh and pays GST on those purchases, the GST amount can be claimed as Input Tax Credit. This significantly reduces the final tax burden. Interstate Business Allowed Businesses can freely sell products and services across India. This is particularly beneficial for: Online sellers Manufacturers Service providers Export-oriented businesses Better Business Credibility Corporate clients often prefer dealing with GST-registered suppliers who can issue tax invoices and provide Input Tax Credit benefits. This can directly impact business opportunities. Understanding the GST Composition Scheme The Composition Scheme was introduced to reduce the compliance burden for small taxpayers. Instead of following regular GST procedures, eligible businesses can pay tax at a fixed lower rate based on turnover. The scheme is primarily designed for: Small traders Local retailers Small restaurants Certain service providers Key Features of Composition Scheme Simplified Compliance Businesses generally face: Reduced recordkeeping requirements Simpler return filing Less administrative burden This is attractive for small businesses with limited accounting resources. Lower Tax Rates Composition taxpayers typically pay tax at prescribed composition rates rather than normal GST rates. However, lower tax rates do not always mean lower overall tax costs. The impact depends on Input Tax Credit eligibility and business model. No Input Tax Credit This is the biggest limitation. Composition dealers: Cannot claim Input Tax Credit Cannot pass ITC benefits to customers For many businesses, this can significantly affect competitiveness. GST Registration vs Composition Scheme: Detailed Comparison Factor Regular GST Registration Composition Scheme Input Tax Credit Available Not Available Interstate Sales Allowed Restricted in many cases E-commerce Selling Allowed Limited GST Invoice Allowed Not Allowed as Tax Invoice Compliance Higher Lower Growth Flexibility High Limited Corporate Clients Preferred Less Preferred Tax Administration Detailed Simplified Who Should Choose Regular GST Registration? Regular GST registration is usually ideal for businesses that: Plan to Grow Aggressively If you expect turnover growth over the next few years, switching later may create operational disruptions. Starting with regular registration can be more practical. Sell to Businesses B2B customers prefer vendors who can provide Input Tax Credit benefits. Without ITC benefits, customers may prefer competitors. Operate Online Businesses selling through: Amazon Flipkart Meesho Other marketplaces typically require regular GST registration. Have Significant Purchase Costs When businesses purchase inventory, machinery, or raw materials regularly, Input Tax Credit becomes highly valuable. This often outweighs the compliance burden. Who Should Choose the Composition Scheme? The composition scheme may work well for: Local Retail Shops Businesses serving local consumers often find compliance simplicity attractive. Examples: Grocery stores Gift shops Local traders Small retail outlets Businesses with Minimal Input Tax Credit Requirements If purchase-related GST is relatively low, losing ITC may have limited impact. Owners Seeking Simpler Compliance For business owners who prefer a straightforward taxation framework, composition can reduce administrative workload. Real-Life Bhopal Business Examples Example 1: Local Grocery Store Annual Turnover: ₹60 lakh Customer Base: Local consumers Interstate Sales: None ITC Requirement: Low Recommended Option: Composition Scheme Reason: Compliance simplicity may outweigh ITC benefits. Example 2: Manufacturing Unit Annual Turnover: ₹1.2 crore Raw Material Purchases: High B2B Customers: Yes Recommended Option: Regular GST Registration Reason: Input Tax Credit benefits can significantly reduce tax costs. Example 3: Digital Marketing Agency Annual Turnover: ₹45 lakh Clients Across India Growing Business Recommended Option: Regular GST Registration Reason: Interstate services and future growth make regular registration more suitable. Example 4: Restaurant Business Annual Turnover: ₹75 lakh Local Customer Base Limited Expansion Plans Recommended Option: Depends on cost structure and tax planning analysis. Professional evaluation is recommended. Common Mistakes Businesses Make Choosing Based Only on Tax Rate Many business owners focus only on lower composition rates and ignore ITC losses. Ignoring Growth Plans A scheme suitable today may become restrictive within a year. Not Evaluating Customer Type B2B and B2C businesses often require different GST strategies. Poor Record Keeping Regardless of the chosen scheme, proper documentation remains essential. How to Switch Between Schemes Businesses may switch between schemes if eligibility conditions are met. Before switching: Review turnover projections Analyze customer profile Estimate ITC benefits Evaluate compliance costs Consult a GST professional A structured analysis prevents costly mistakes. Expert Recommendation from Chartered Accountants In our experience advising businesses across Bhopal, most growth-oriented businesses benefit more from Regular GST Registration. While the Composition Scheme provides simplicity,

Startup Compliance Checklist for New Businesses in Bhopal: A CA’s Complete Guide

TL;DR Starting a business involves much more than registering a company and opening a bank account. Every startup must comply with multiple legal, tax, accounting, and regulatory requirements to avoid penalties and build a sustainable business. Essential Startup Compliance Checklist ✔ Business Registration ✔ PAN & TAN Registration ✔ GST Registration (if applicable) ✔ MSME/Udyam Registration ✔ Professional Accounting System ✔ Bookkeeping & Record Maintenance ✔ Income Tax Compliance ✔ TDS Compliance ✔ Labour Law Compliance ✔ Annual Filings & Regulatory Reporting Businesses that establish compliance systems from day one are better positioned for growth, funding, and long-term success. Why Startup Compliance Matters Many entrepreneurs focus entirely on product development, customer acquisition, and revenue generation during the initial stages of business. While these activities are important, ignoring compliance can become one of the costliest mistakes a startup makes. Poor compliance can lead to: Government penalties Tax notices GST disputes Loss of input tax credits Regulatory action Difficulty obtaining funding Banking and loan challenges Reputational risks On the other hand, businesses with strong compliance frameworks gain greater credibility with investors, banks, customers, and government agencies. Compliance is not merely a legal obligation—it is a business growth strategy. Startup Compliance Checklist Overview The startup compliance process can be divided into five major categories: Compliance Area Importance Business Registration Legal identity Tax Compliance Avoid penalties Accounting Compliance Financial transparency Labour Compliance Employee protection Annual Filings Regulatory compliance Let’s examine each area in detail. 1. Business Registration Requirements Choosing the right business structure is the first compliance decision every entrepreneur must make. Common business structures include: Sole Proprietorship Suitable for: Small businesses Freelancers Consultants Advantages: Easy setup Lower compliance burden Limitations: Unlimited liability Partnership Firm Suitable for: Family businesses Professional firms Joint ventures Advantages: Shared ownership Flexible management Limitations: Partner liability exposure LLP (Limited Liability Partnership) Suitable for: Professional service firms Growing startups Advantages: Limited liability Simplified compliance Private Limited Company Suitable for: Fundraising startups High-growth businesses Technology ventures Advantages: Investor-friendly structure Limited liability Greater credibility Essential Registration Documents Regardless of business structure, startups generally require: PAN Aadhaar Address proof Bank account Business address documentation Identity proof of promoters Proper documentation ensures smoother registration and future compliance. 2. PAN and TAN Registration PAN (Permanent Account Number) PAN serves as the primary tax identification number for businesses. It is required for: Opening business bank accounts Filing tax returns Financial transactions Regulatory compliance TAN (Tax Deduction and Collection Account Number) Businesses responsible for deducting tax at source must obtain TAN. TAN becomes necessary when: Salaries are paid Contractors are engaged Professional fees are paid Certain specified payments are made Failure to comply with TDS regulations can attract penalties and interest. 3. GST Registration Requirements One of the most important startup compliance requirements involves GST. GST Registration May Be Required For: Businesses crossing prescribed turnover thresholds Interstate suppliers E-commerce sellers Certain service providers Businesses voluntarily opting into GST Benefits of GST Registration Legal compliance Input Tax Credit eligibility Improved credibility Business expansion opportunities Common GST Compliance Requirements GST registration Tax invoice generation Return filing Input tax credit reconciliation Record maintenance Many startups underestimate GST compliance complexity and face avoidable issues later. 4. MSME/Udyam Registration Many entrepreneurs overlook one of the most beneficial registrations available to small businesses. Benefits of Udyam Registration Easier loan approvals Government scheme eligibility Subsidies and incentives Reduced compliance burden in certain areas Protection against delayed payments For eligible businesses, Udyam registration should be completed early. 5. Startup Accounting and Bookkeeping Compliance Accounting is one of the most neglected compliance areas among new businesses. Unfortunately, poor accounting often creates: Tax issues GST mismatches Cash flow problems Funding challenges Essential Accounting Requirements Maintain records of: Sales invoices Purchase invoices Expenses Bank transactions Payroll records GST records Asset registers Best Practice Implement accounting software from day one rather than attempting to reconstruct records later. Why Proper Bookkeeping Matters Accurate bookkeeping helps startups: Monitor profitability Manage cash flow Prepare tax returns Secure investments Support audits Improve decision-making Investors and lenders often review financial records before approving funding. Poor bookkeeping can negatively affect business valuation and credibility. 6. Income Tax Compliance Every business must understand its income tax obligations. Key requirements include: Income Tax Return Filing Businesses must file tax returns within applicable deadlines. Advance Tax Certain businesses may need to pay taxes periodically throughout the year. Tax Planning Proper tax planning helps: Reduce tax liability legally Improve cash flow Avoid year-end surprises Startups that ignore tax planning often pay more tax than necessary. 7. TDS Compliance Many startups are unaware of Tax Deducted at Source (TDS) obligations. TDS may apply when making payments such as: Salaries Contractor payments Professional fees Rent Commission Compliance generally includes: Deduction of tax Deposit of deducted tax Filing TDS returns Issuing certificates TDS defaults can result in penalties and compliance notices. 8. Labour Law Compliance Businesses employing staff must also address labour-related obligations. Depending on employee strength and business activities, requirements may include: Employment contracts Payroll records Employee benefits Statutory registrations Labour law reporting Maintaining proper HR documentation protects both employers and employees. 9. Annual Compliance Requirements Compliance does not end after registration. Businesses must continue meeting ongoing obligations. Common Annual Requirements Income tax return filing Financial statement preparation GST filings TDS filings Regulatory filings Accounting reviews Audit requirements (where applicable) Missing deadlines can result in penalties and legal complications. Common Startup Compliance Mistakes Many startups make avoidable compliance mistakes during their first few years. Mistake 1 Delaying GST registration. Mistake 2 Not maintaining accounting records. Mistake 3 Missing tax filing deadlines. Mistake 4 Mixing personal and business finances. Mistake 5 Ignoring TDS obligations. Mistake 6 Choosing the wrong business structure. Mistake 7 Trying to manage compliance without professional guidance. These mistakes often become expensive as the business grows. How a Chartered Accountant Can Help Startup founders already manage multiple responsibilities. A Chartered Accountant helps ensure compliance remains under control. Professional support typically includes: Business registration guidance GST registration and compliance Tax planning Accounting setup Bookkeeping support Financial reporting Regulatory compliance

Common Accounting Mistakes That Cost Small Businesses Thousands in Taxes

TL;DR Many small businesses lose significant amounts of money every year—not because of poor sales, but because of poor accounting. The most expensive accounting mistakes include: ✔ Mixing personal and business finances ✔ Missing deductible expenses ✔ Poor bookkeeping ✔ Incorrect GST records ✔ Delayed financial reporting ✔ Poor cash flow monitoring ✔ Weak tax planning ✔ Lack of professional accounting oversight Avoiding these mistakes can improve profitability, reduce tax liability, and strengthen long-term business growth. Why Accounting Matters More Than Most Business Owners Realize Many entrepreneurs focus heavily on sales, marketing, and operations. However, accounting is often the foundation that determines whether a business grows profitably or struggles financially. Good accounting helps business owners: Understand profitability Manage taxes efficiently Monitor cash flow Make informed decisions Avoid penalties Secure loans and investments Scale operations confidently Unfortunately, many small businesses treat accounting as a year-end activity rather than an ongoing business function. This mistake can be extremely costly. The Hidden Cost of Poor Accounting Accounting errors rarely create immediate problems. Instead, they gradually affect: Tax liability Business profitability Compliance status Cash flow Financial planning For example, a business that fails to record deductible expenses throughout the year may pay significantly more tax than necessary. Similarly, inaccurate financial records can trigger GST mismatches, compliance notices, and unnecessary scrutiny. The true cost often extends far beyond accounting fees. 1. Mixing Personal and Business Finances This is one of the most common mistakes among small business owners. Many entrepreneurs use the same bank account for: Business purchases Personal expenses Family spending Vendor payments This creates confusion and makes accurate accounting nearly impossible. Consequences Inaccurate financial statements Lost deductible expenses Tax filing complications Audit risks Best Practice Maintain separate: Bank accounts Credit cards Expense records for business and personal use. 2. Ignoring Regular Bookkeeping Many businesses postpone bookkeeping until tax season. Unfortunately, delayed bookkeeping often results in: Missing transactions Incorrect records Forgotten expenses Financial confusion Example A retailer with hundreds of monthly transactions may struggle to reconstruct records months later. The result is inaccurate reporting and lost tax deductions. Best Practice Update accounting records weekly or monthly. Consistent bookkeeping improves financial accuracy and decision-making. 3. Failing to Record Business Expenses Properly Every legitimate business expense should be documented appropriately. Commonly missed expenses include: Travel costs Professional subscriptions Office supplies Software expenses Communication costs Business meals Training expenses Impact When expenses are not recorded properly: Taxable income appears higher Tax liability increases Profit figures become misleading This is one of the easiest ways businesses unintentionally overpay taxes. 4. Poor GST Record Management GST compliance depends heavily on accurate accounting records. Many businesses make mistakes involving: Tax invoices GST classifications Input tax records Filing reconciliations Consequences Poor GST accounting can lead to: Input Tax Credit losses Compliance notices Interest liabilities Penalties Best Practice Reconcile GST records regularly and maintain accurate supporting documentation. 5. Not Reconciling Bank Accounts Bank reconciliation ensures accounting records match actual bank transactions. Without reconciliation: Duplicate entries go unnoticed Missing transactions remain hidden Fraud risks increase Cash balances become unreliable Recommended Frequency Monthly reconciliation is generally considered a minimum best practice. 6. Delaying Accounting Entries Many business owners record transactions weeks or months after they occur. Delayed accounting creates: Inaccurate reports Decision-making problems Tax planning difficulties Compliance risks Real-time accounting provides a far clearer picture of business performance. 7. Ignoring Cash Flow Management Profitability and cash flow are not the same thing. A business may appear profitable on paper while struggling to pay suppliers and employees. Common Cash Flow Mistakes Excessive credit sales Delayed collections Poor inventory management Lack of forecasting Best Practice Monitor: Incoming cash Outgoing cash Outstanding receivables Upcoming liabilities on a regular basis. 8. Poor Tax Planning Throughout the Year Many businesses only think about taxes when filing returns. This reactive approach limits tax-saving opportunities. Effective tax planning should occur throughout the financial year. Benefits Lower tax liability Better cash flow management Improved compliance Reduced year-end stress Tax planning is most effective when integrated into routine financial management. 9. Inaccurate Inventory Accounting For businesses dealing with physical products, inventory accounting directly affects profitability and taxation. Common mistakes include: Incorrect stock counts Outdated inventory records Inventory valuation errors Unrecorded losses Impact Inventory errors can distort: Profit calculations Taxable income Financial statements Accurate inventory controls are essential. 10. Trying to Manage Everything Without Professional Support Many business owners attempt to handle accounting themselves despite limited expertise. While this may appear cost-effective initially, it often becomes expensive later. Professional accountants can help identify: Tax-saving opportunities Compliance risks Financial inefficiencies Reporting errors Their expertise often saves businesses significantly more than the cost of professional services. How Accounting Errors Increase Tax Liability Many accounting mistakes directly affect tax outcomes. Accounting Error Potential Impact Missing expenses Higher taxable income Poor bookkeeping Incorrect tax reporting GST errors Penalties and interest Inventory mistakes Misstated profits Delayed accounting Missed tax planning opportunities Incomplete records Lost deductions The cumulative financial impact can be substantial over time. How to Build an Error-Free Accounting System Business owners can reduce accounting risks by implementing a structured process. Step 1 Maintain separate financial accounts. Step 2 Use accounting software. Step 3 Update records consistently. Step 4 Perform monthly reconciliations. Step 5 Track expenses systematically. Step 6 Review GST compliance regularly. Step 7 Conduct quarterly financial reviews. Step 8 Work with qualified accounting professionals. These steps create stronger financial controls and better decision-making capabilities. Benefits of Professional Accounting Services Professional accounting support provides advantages beyond compliance. Better Tax Efficiency Proper accounting helps identify legitimate deductions and planning opportunities. Improved Cash Flow Accurate financial information supports better operational decisions. Stronger Compliance Professional oversight reduces the risk of notices and penalties. Better Business Growth Reliable financial data enables confident expansion and investment decisions. Reduced Stress Business owners can focus on growth while professionals manage financial compliance. Conclusion Accounting mistakes are not merely administrative errors—they can directly affect profitability, tax liability, compliance, and long-term business success. Small businesses that neglect bookkeeping, fail to track expenses, ignore reconciliations, or

Expert Insights: Tax Planning Strategies Every Bhopal Business Owner Should Know in 2026

TL;DR If you’re running a business in Bhopal, tax planning should not be a year-end activity. The most successful businesses plan taxes throughout the financial year. In 2026, rising compliance requirements, stricter GST monitoring, and increased data matching between government systems make proactive tax planning more important than ever. Key strategies include: ✔ Choosing the correct business structure ✔ Maximizing deductible business expenses ✔ Managing GST Input Tax Credit efficiently ✔ Planning advance tax payments ✔ Using depreciation benefits strategically ✔ Conducting quarterly tax reviews ✔ Maintaining proper documentation ✔ Working with an experienced Chartered Accountant Businesses that implement these strategies can improve profitability, reduce tax liabilities legally, and minimize compliance risks. Why Tax Planning Matters More Than Ever in 2026 Business taxation in India continues to evolve. Authorities now have access to more integrated financial data than ever before. GST filings, TDS returns, bank transactions, annual returns, and income tax filings are increasingly interconnected. For business owners in Bhopal, this means two things: Non-compliance is easier to detect. Proper tax planning creates larger financial advantages. Many entrepreneurs still confuse tax planning with last-minute tax saving. However, effective tax planning is a year-round financial strategy designed to: Reduce tax liability legally Improve cash flow Enhance profitability Prevent penalties Support business growth Businesses that plan proactively often retain more capital for expansion, hiring, technology upgrades, and working capital needs. Tax Planning vs Tax Evasion: Understanding the Difference Before discussing strategies, it is important to understand the distinction. Tax Planning Tax Evasion Legal Illegal Uses available provisions under law Conceals income Supported by documentation Misrepresents transactions Reduces risk Increases legal exposure Long-term benefit Short-term risk Professional tax planning focuses entirely on legal methods permitted under Indian tax laws. The objective is not avoiding tax—it is paying only what is legally required. Common Tax Mistakes Bhopal Businesses Still Make Despite increasing awareness, many businesses continue to make costly mistakes. Delaying Tax Planning Until March Waiting until the financial year-end limits available options. Missing Eligible Deductions Numerous businesses fail to claim legitimate expenses due to poor recordkeeping. Improper GST Reconciliation Unmatched GST data often leads to denied Input Tax Credits. Inadequate Documentation Lack of supporting documents can result in rejected claims during assessments. Incorrect Business Structure Many growing businesses continue operating under structures that are no longer tax efficient. Avoiding these mistakes can significantly improve financial outcomes. 10 Tax Planning Strategies Every Business Owner Should Implement 1. Choose the Right Business Structure The structure of your business directly impacts taxation. Common structures include: Proprietorship Partnership Firm LLP Private Limited Company As businesses grow, their original structure may become less tax efficient. For example, a rapidly expanding proprietorship may benefit from restructuring into an LLP or Private Limited Company. Regular evaluation ensures your structure aligns with current business objectives and tax requirements. 2. Track Every Eligible Business Expense One of the easiest ways to reduce taxable income is by properly recording legitimate business expenses. Common deductible expenses include: Office rent Salaries and wages Internet and communication expenses Professional fees Marketing costs Travel expenses Business software subscriptions Insurance premiums Many businesses unknowingly overpay taxes simply because expenses are poorly documented. A robust accounting system ensures every eligible deduction is captured. 3. Optimize Depreciation Benefits Depreciation remains one of the most valuable tax planning tools available. Assets such as: Machinery Computers Office equipment Furniture Vehicles can generate significant tax benefits over their useful life. Strategic timing of asset purchases can help businesses maximize depreciation claims while improving operational efficiency. For manufacturing and trading businesses in Bhopal, this strategy can create substantial tax savings. 4. Improve GST Input Tax Credit Management GST Input Tax Credit (ITC) continues to be one of the most underutilized tax-saving opportunities. To maximize ITC: Verify supplier compliance Match invoices regularly Conduct monthly reconciliations Monitor GSTR filings Resolve mismatches immediately Failure to manage ITC properly can increase tax costs unnecessarily. Businesses that actively monitor GST records often discover recoverable credits that improve cash flow. 5. Plan Advance Tax Payments Carefully Advance tax is not merely a compliance requirement. It is also a financial planning tool. Benefits include: Better cash flow management Reduced interest liability Improved forecasting Avoidance of penalties Instead of reacting to tax obligations, successful businesses forecast taxable income throughout the year and plan accordingly. 6. Maximize Available Deductions Many businesses fail to utilize deductions available under various provisions of tax law. Potential opportunities may include: Employee benefit contributions Research and development expenses Startup incentives Business loan interest Professional development costs Each business has unique eligibility criteria. Regular consultation with a Chartered Accountant helps identify opportunities specific to your industry. 7. Maintain Proper Documentation Documentation is the foundation of successful tax planning. Maintain records for: Invoices Contracts Bank statements GST returns Payroll records Asset registers Expense vouchers Strong documentation not only supports deductions but also simplifies audits and assessments. Think of documentation as your first line of defense against compliance issues. 8. Leverage Technology and Accounting Automation Manual bookkeeping increases the risk of errors. Modern accounting solutions provide: Real-time reporting Automated GST calculations Expense tracking Tax forecasting Compliance alerts Technology enables business owners to identify tax-saving opportunities earlier and make informed financial decisions. Automation also improves accuracy and operational efficiency. 9. Review Related Party Transactions Businesses frequently engage in transactions involving: Family-owned entities Sister concerns Group companies Improper structuring can attract scrutiny. Ensure: Transactions occur at reasonable values Agreements are documented Supporting evidence is maintained Proper planning reduces compliance risk while maintaining operational flexibility. 10. Conduct Quarterly Tax Health Checks The best businesses do not wait until year-end. They review their tax position every quarter. Quarterly reviews help identify: Tax-saving opportunities Compliance gaps Cash flow concerns GST mismatches Documentation deficiencies A proactive review process prevents surprises and supports better decision-making. Industry-Specific Tax Planning Tips Manufacturers Focus on: Depreciation planning Inventory valuation Input tax credit optimization Capital expenditure timing Retail Businesses Prioritize: GST reconciliation Inventory management Cash flow forecasting Expense tracking Service Providers Pay close attention to: Professional income reporting Advance tax calculations

The Real Cost of Running a Business in India: Registration, GST, Tax, Accounting & Hidden Expenses

TL;DR Many businesses in India face financial challenges not because of insufficient revenue, but because key costs are underestimated during planning and growth stages. Key cost drivers include: Business registration and entity structure decisions GST and tax compliance obligations Accounting and bookkeeping systems Operational overheads and administrative expenses Hidden financial inefficiencies and cash flow gaps Understanding the complete cost structure of a business is essential for sustainable growth and long-term stability. Why Business Costs Are Often Miscalculated Many entrepreneurs focus heavily on revenue opportunities while underestimating the financial commitments required to operate and grow a business. A business may appear profitable on paper but still experience financial pressure due to: Delayed receivables Compliance-related obligations Limited financial visibility Untracked operational expenses Inefficient cash flow management One common challenge businesses face is inadequate visibility into spending patterns and financial obligations. The Core Cost Components of Running a Business in India 1. Business Registration Costs and Structural Setup Every business begins with registration, but the chosen business structure can influence long-term compliance requirements, taxation, and operational flexibility. Key elements influencing cost structure include: Entity type selection Documentation and registration requirements Legal and regulatory formalities Initial compliance setup Common business structures include: Proprietorship (simplified structure for small businesses) Partnership Firm (shared ownership model) Limited Liability Partnership (LLP) Private Limited Company Selecting an unsuitable business structure may result in: Additional compliance requirements Increased administrative effort Operational limitations as the business grows 2. GST & Tax Compliance Costs Tax compliance and related obligations are often overlooked during business planning. Key components may include: GST registration and return filing Input tax credit reconciliation TDS compliance and reporting Advance tax planning Annual income tax filings Business Impact Areas Working capital management Cash flow timing Administrative workload Compliance-related risks The complexity of GST compliance may increase for businesses involved in: Multi-state operations Ecommerce activities High transaction volumes Multiple business verticals 3. Accounting & Bookkeeping Systems Accounting serves as the financial foundation of a business and supports informed decision-making. Core elements include: Transaction recording systems Expense classification and tracking Invoice management Bank reconciliations Periodic financial reporting Without structured accounting processes: Expense visibility may be reduced Profitability analysis becomes difficult Financial decision-making may become reactive Well-maintained accounting records can help improve financial clarity, compliance readiness, and operational control. 4. Legal & Statutory Compliance Businesses operate within various regulatory frameworks that require periodic compliance. Examples include: ROC filings for companies and LLPs Annual returns Labor law compliance requirements Industry-specific registrations and licenses Audit-related documentation Failure to comply with applicable regulations may result in: Administrative challenges Regulatory notices Operational disruptions 5. Operational Overheads Operational expenses extend beyond direct revenue-generating activities. Common overhead costs include: Employee-related expenses Office and infrastructure costs Software and technology subscriptions Vendor and service provider payments Logistics and distribution expenses These costs often evolve as the business expands and therefore require regular monitoring. Hidden Costs Most Founders Miss Many business owners focus on visible expenses while overlooking indirect costs that can affect profitability. Common Hidden Cost Categories Inefficient vendor agreements Delayed receivables Manual processing errors Duplicate operational activities Poor inventory control Limited tax planning Rework caused by inaccurate records Although these costs may not always appear as direct expenses, they can influence overall financial performance. Monthly vs Annual Financial Burden Breakdown Category Frequency Impact Area Tax filings Monthly / Quarterly Compliance management Accounting updates Monthly Financial reporting GST reconciliation Monthly Cash flow accuracy ROC compliance Annual Regulatory requirements Operational expenses Ongoing Profitability and growth Why Businesses Experience Cash Flow Pressure Cash flow challenges are often linked to financial structure and timing rather than profitability alone. Common reasons include: Delayed customer payments Tax payment schedules Untracked expenses Inventory holding costs Inadequate forecasting Even profitable businesses may experience liquidity constraints when cash inflows and outflows are not properly aligned. Financial Planning Mistakes in Early-Stage Businesses Some common financial planning challenges include: Lack of cost forecasting Ignoring compliance timelines Mixing personal and business finances Irregular financial reviews Absence of accounting discipline These issues may accumulate over time and become more visible as the business scales. How Accounting Systems Reduce Cost Leakage Structured accounting systems support stronger financial management by: Recording transactions accurately Improving expense visibility Supporting tax compliance Enhancing cash flow planning Strengthening internal controls Greater financial clarity can contribute to better business decisions and improved resource allocation. Realistic Cost Structure Framework for SMEs A stable business typically allocates resources across: Compliance and regulatory obligations Accounting and financial management systems Operational infrastructure Taxation responsibilities Growth and expansion initiatives The objective is not to eliminate costs entirely but to optimize resources through effective planning and monitoring. Conclusion The cost of running a business in India extends beyond registration expenses. It involves ongoing compliance obligations, taxation requirements, accounting systems, operational overheads, and financial management processes. Businesses that do not establish structured financial systems at an early stage may encounter: Cash flow challenges Compliance-related pressure Growth constraints Limited financial visibility A well-organized financial framework can help businesses improve clarity, stability, and long-term scalability. Frequently Asked Questions 1. What is the real cost of running a business in India? The overall cost includes registration expenses, taxation compliance, accounting systems, operational overheads, technology costs, and various administrative requirements. 2. What are hidden business expenses? Hidden expenses may include delayed receivables, inefficient processes, bookkeeping errors, compliance lapses, and untracked operational costs. 3. Why do businesses underestimate costs? Many businesses focus primarily on revenue opportunities and may not fully account for compliance obligations, operational overheads, and financial management requirements. 4. Is GST a major cost for small businesses? GST itself is a tax mechanism, but compliance requirements associated with GST can influence administrative workload, cash flow planning, and financial processes. 5. What is the biggest expense in running a business? Major expenses vary by industry and business model. However, operational, employee-related, compliance, and infrastructure costs often represent significant ongoing expenditures. 6. How can businesses reduce financial pressure? Businesses can improve financial control through structured accounting systems, regular financial reviews, effective compliance management, and proper cash flow planning. 7. Do